In a world where financial responsibilities often feel overwhelming, having a budget is not just a luxury it’s a necessity. Budgeting serves as a roadmap, guiding you toward financial stability and success. It ensures that every dollar you earn is working effectively, helping you meet your needs, manage your wants, and prepare for the future.

Financial planning is critical in daily life. Without it, money can easily slip through your fingers, leaving you unprepared for unexpected expenses or long-term goals. A budget provides structure, showing you where your money is going and how to allocate it wisely. It’s not about limiting your spending; instead, it’s about empowering you to spend with purpose.

A well-thought-out budget also lays the foundation for achieving your financial goals. Whether you’re saving for a down payment on a house, paying off debt, or building an emergency fund, budgeting ensures that your goals are more than just dreams; they become achievable milestones. By breaking down these aspirations into manageable steps, a budget helps you track progress and stay motivated.

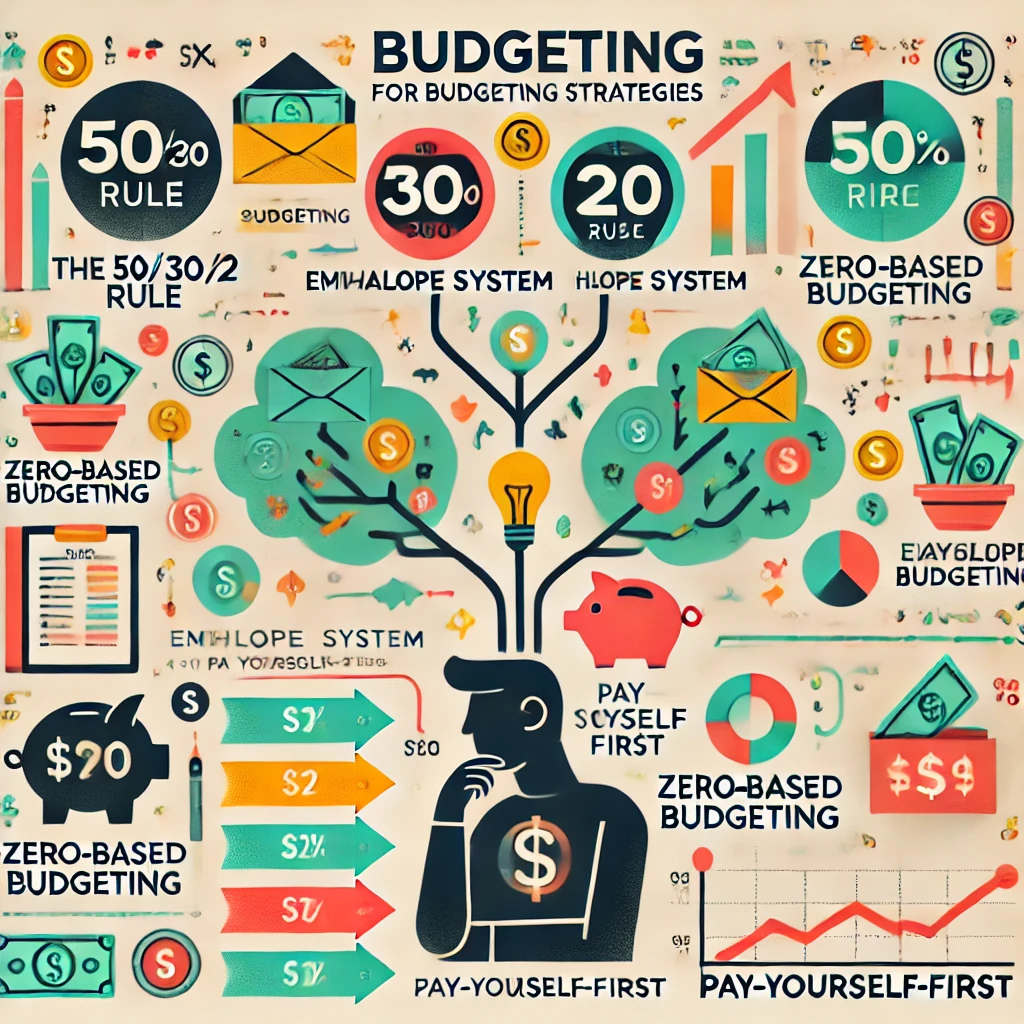

What makes budgeting even more effective is its flexibility. Different strategies cater to different financial situations and personalities. For example, if you prefer simplicity, the 50/30/20 rule might be a good fit. If you want detailed control, zero-based budgeting could be your answer. Understanding these options allows you to choose a method that complements your lifestyle and financial habits.

Budgeting is not a one-size-fits-all solution, but its universal benefits are undeniable. It provides clarity, reduces stress, and puts you in control of your finances. As you explore the various strategies available, you’ll discover that budgeting isn’t just about money—it’s about building a life that reflects your values and priorities.

Understanding Your Financial Goals

A successful budget starts with a clear understanding of your financial goals. These goals act as the foundation of your budgeting strategy, guiding how you allocate your resources and prioritize your spending.

Short-Term vs. Long-Term Goals

Financial goals can generally be divided into two categories: short-term and long-term. Short-term goals are those you aim to achieve within a year or two. These might include building an emergency fund, paying off a small debt, or saving for a vacation. They’re often specific, time-sensitive, and easier to track, making them a great starting point for budgeting.

Long-term goals, on the other hand, require sustained effort over several years or even decades. Examples include saving for retirement, purchasing a home, or funding a child’s education. These goals typically involve larger sums of money and require more complex planning. A robust budget can help you consistently allocate funds to these objectives, ensuring you stay on track without sacrificing your immediate needs.

Assessing Your Priorities

Once you’ve outlined your goals, it’s essential to prioritize them. Not all financial goals carry the same weight, and your budget should reflect what matters most to you. For instance, if you’re juggling credit card debt and an aspiration to travel, addressing high-interest debt should take precedence. This approach not only improves your financial health but also frees up resources for future aspirations.

Similarly, if you’re aiming to grow wealth through investments, you may need to prioritize building a sufficient savings cushion first. This ensures you’re prepared for unexpected expenses without having to withdraw from your investments prematurely.

Aligning Budgeting with Your Lifestyle

A budget is most effective when it fits seamlessly into your lifestyle. Are you someone who thrives on structure, or do you prefer flexibility? For example, if you value detailed oversight of your finances, zero-based budgeting may be ideal as it requires assigning every dollar a purpose. Alternatively, if you prefer simplicity, the 50/30/20 rule offers a more relaxed approach while still encouraging discipline.

Your spending habits also play a role in how you structure your budget. If you’re prone to impulse purchases, methods like the envelope system, which uses cash limits for categories, can help curb overspending. Conversely, if you have irregular income, a percentage-based budgeting approach can ensure your priorities are met regardless of fluctuations.

By aligning your budgeting strategy with your financial goals and lifestyle, you create a sustainable plan that feels natural rather than restrictive. The better your budget reflects your personal priorities and habits, the more likely you are to stick with it—and the closer you’ll be to achieving both short-term wins and long-term success.

Popular Budgeting Strategies

When it comes to managing your money, there’s no shortage of budgeting strategies. Each method offers unique benefits, catering to different financial situations, habits, and goals. Let’s explore some of the most popular approaches to help you find the one that fits your needs.

The 50/30/20 Rule

The 50/30/20 rule is one of the simplest and most accessible budgeting methods. It divides your income into three categories:

- 50% for essentials: Rent or mortgage, utilities, groceries, transportation, and other necessities.

- 30% for wants: Entertainment, dining out, hobbies, and discretionary spending.

- 20% for savings and debt repayment: Emergency fund contributions, retirement savings, and paying off loans.

This strategy is particularly suited for beginners or individuals with a steady income. It provides a clear framework that balances necessary expenses with enjoyment and future planning. By focusing on percentages, it’s easy to adapt to different income levels without overcomplicating your budget.

Zero-Based Budgeting

Zero-based budgeting (ZBB) involves assigning every dollar of your income a specific purpose. At the end of the budgeting process, your income minus expenses should equal zero. This method requires you to track all spending meticulously, ensuring that no money is unaccounted for.

For instance, if you earn $3,000 in a month, every dollar whether allocated to bills, savings, or leisure must be planned.

This strategy is ideal for those who want detailed control over their finances and are willing to put in the effort to track spending. It’s particularly effective for people looking to maximize savings, reduce wasteful expenses, or work toward specific financial goals.

Envelope System

The envelope system is a cash-based budgeting method where you physically divide money into envelopes for each spending category (e.g., groceries, dining out, transportation). Once the money in an envelope is gone, you stop spending in that category until the next budgeting cycle.

This approach is excellent for individuals who prefer tangible spending limits and struggle with overspending on credit or debit cards. It also encourages mindful spending and helps avoid unnecessary debt. While the envelope system is traditionally cash-based, modern apps replicate this concept digitally for added convenience.

Pay-Yourself-First Method

In the pay-yourself-first method, you prioritize savings and investments before addressing other expenses. As soon as you receive your income, a predetermined amount is set aside for savings or financial growth, leaving the remainder for bills and discretionary spending.

This strategy is particularly effective for individuals focused on building wealth, preparing for retirement, or achieving ambitious financial goals. It instills the habit of prioritizing your future over immediate wants and can be combined with other budgeting methods for a comprehensive approach.

Percentage-Based Budgeting

Percentage-based budgeting is similar to the 50/30/20 rule but allows for more customization. Instead of sticking to predefined percentages, you allocate your income based on your unique priorities. For example:

- 70% for living expenses

- 20% for savings/investments

- 10% for leisure or discretionary spending

This method is particularly useful for those with variable income, such as freelancers or small business owners. By adjusting percentages based on your income flow, you can maintain financial stability while ensuring your priorities are met.

Assessing Your Income and Expenses

Before diving into any budgeting strategy, it’s crucial to understand your financial situation. Start by tracking your monthly income, including your salary, freelance earnings, or any other sources. Next, categorize your expenses into fixed costs, such as rent, utilities, and insurance, and variable costs, like groceries, entertainment, and dining out.

Tracking your expenses can reveal spending leaks—areas where money slips away unnoticed. For instance, small daily purchases, like coffee or snacks, can add up over time. Identifying these leaks allows you to make informed decisions about where to cut back.

Finally, don’t overlook the importance of an emergency fund. Setting aside 3–6 months’ worth of living expenses provides a safety net for unexpected situations, such as medical emergencies or job loss. An emergency fund is the foundation of financial security and should be a priority in your budgeting efforts.

Tailoring the Strategy to Your Lifestyle

Your budget should reflect your unique lifestyle, values, and goals. Consider factors such as your income level, the nature of your expenses, and your personality. For example, if you prefer flexibility, the 50/30/20 rule might suit you better. If you thrive on structure, zero-based budgeting may be a better fit.

Balancing flexibility with discipline is key. While a budget should provide guidance, it shouldn’t feel overly restrictive. Hybrid approaches, like combining the 50/30/20 rule with the envelope system, can offer the best of both worlds. For instance, use the 50/30/20 framework for high-level planning and envelopes for categories prone to overspending, like dining out.

Common Challenges and How to Overcome Them

Budgeting is not without its challenges, but with preparation, you can overcome them. Staying consistent can be tough, especially during busy periods. To stay on track, set reminders and schedule regular budget reviews.

Irregular income or unexpected expenses can disrupt even the best-laid plans. In these cases, a percentage-based budget or maintaining a robust emergency fund can provide stability. Additionally, emotional spending buying to relieve stress or boost mood can derail progress. Recognize triggers for emotional spending and find healthier ways to cope, such as exercising or seeking support from friends.

Tools and Apps to Simplify Budgeting

Modern technology makes budgeting easier than ever. Apps like Mint, You Need a Budget (YNAB), and PocketGuard allow you to track expenses, set goals, and monitor progress seamlessly.

- Mint: Offers automated expense tracking and insights into spending habits.

- YNAB: Focuses on zero-based budgeting, encouraging you to give every dollar a job.

- PocketGuard: Shows how much you can safely spend after accounting for bills and goals.

While digital tools offer convenience, traditional methods, like spreadsheets or pen-and-paper budgeting, work well for those who prefer simplicity. Choose the tool that aligns with your comfort level and needs.

Monitoring and Adjusting Your Budget

A budget isn’t static; it requires regular reviews to stay effective. Set aside time monthly or quarterly to assess your income, expenses, and progress toward goals. Adjustments may be necessary if your financial situation changes or if your chosen strategy isn’t working as expected.

Celebrate milestones, like paying off debt or reaching a savings goal, to stay motivated. Acknowledging progress reinforces positive habits and keeps you committed to your financial journey.

Read more: Use Your ESTA Visa for America and Enjoy Every Business Trip

Conclusion

Finding the best budgeting strategy is a personal journey that depends on your financial goals, lifestyle, and preferences. Whether you’re drawn to the simplicity of the 50/30/20 rule, the structure of zero-based budgeting, or a hybrid approach, the key is consistency and adaptability. With the right strategy, tools, and mindset, budgeting can transform your relationship with money, helping you build a secure and fulfilling financial future.

By

By